27

MarchPer Stirling Capital Outlook – March

Legendary Fidelity portfolio manager Peter Lynch famously said that “if you spend more than 13 minutes analyzing economic and market forecasts, you’ve wasted 10 minutes.”

We have always taken exception to that statement. However, if you were to replace the phrase “economic and market forecasts” with the words “politics and elections”, we would most enthusiastically endorse Mr. Lynch’s perspective.

That enthusiasm is supported by the lessons from history, which suggest that investment markets largely tend to be politically indifferent, and that attempts to make tactical changes to one’s portfolio in response to the latest poll results or some comment by a candidate on social media is normally a recipe for frustration and underperformance. It is not that politics are entirely irrelevant, it is just that other factors, such as inflation, economic growth rates, monetary policy by the Federal Reserve and corporate profits (as examples) have historically proven to be much more impactful.

If there is a direct relationship between politics and the markets, history suggests it is that investors are happiest when the president is generally unpopular and government is so dysfunctional that it cannot accomplish anything (i.e., potentially make things worse).

The current powerful bull market in equities helps to validate that perspective, as it is hard to imagine a much more dysfunctional political environment than the present, while Trump and Biden have tied each other as the least popular Presidents since at least 1960, with average job approval ratings of only 41%. 1

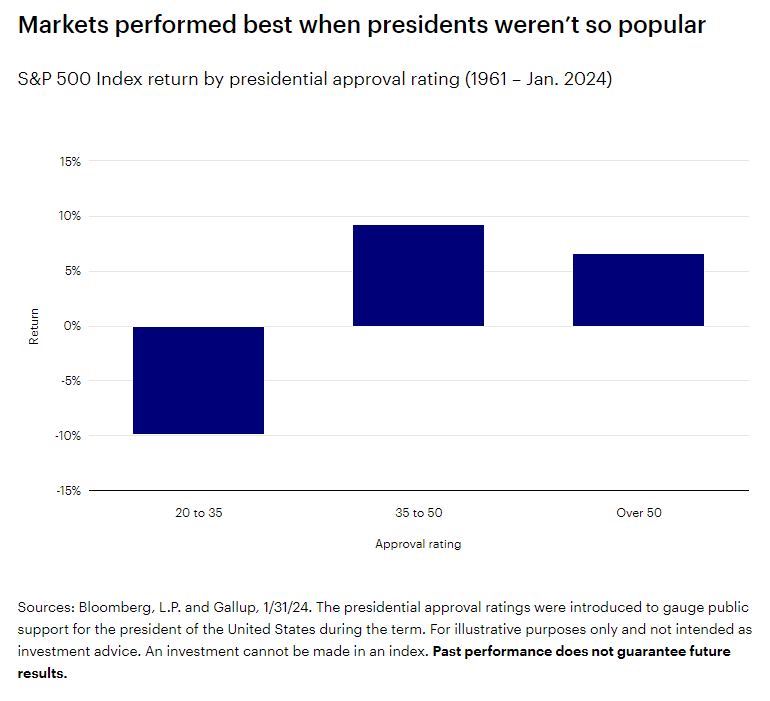

Ironically, relatively unpopular presidential administrations have generally been associated with higher equity market returns. As is illustrated in the above chart of Gallup approval ratings, the Standard and Poor’s 500 Index has historically produced its best returns when the sitting president has approval ratings of between 35% and 50%. Our premise is that it means that the markets don’t want things to be so bad that the economy is in recession and the country is in disarray (likely reflected in approval ratings below 35), but also don’t want a popular president with approval ratings above 50% who has the political capital to get things done (i.e., potentially make things worse). Importantly, investors generally hate uncertainty, and political change adds to uncertainty.

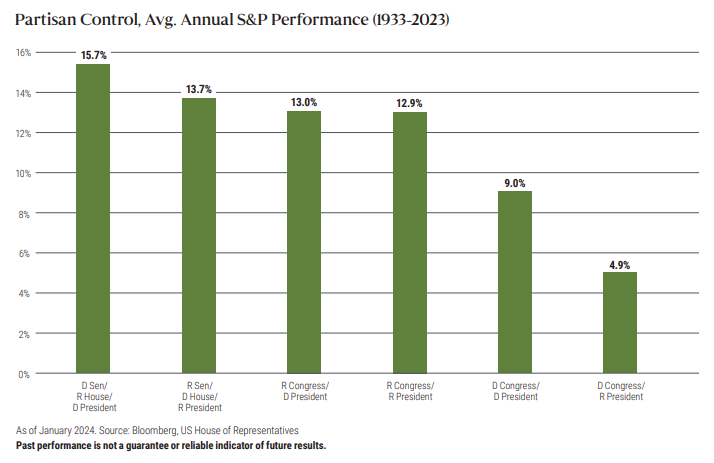

If you buy our premise that markets celebrate ineffective and dysfunctional government, then you should not be in the least bit surprised to learn that the stock market has actually performed much better under divided government than under single-party government, where the same party controls the White House and both branches of Congress.

Indeed, if you look at the data going all of the way back to 1933, the best equity returns have occurred with Democrats in control of the White House and Senate and Republicans in control of the House. The second-best returns have occurred with Republicans in control of the White House and Senate and Democrats in charge of the House, while the third best average returns have occurred with a Democratic president and Republicans in charge of both houses of Congress.

According to Schroders, “since the 1948 presidential election, U.S. equities have posted an average total return of 14.3% when a president has had to deal with a divided Congress, compared with a more modest increase of 13.0% with a unified government. Democratic presidents have posted gains of 18.8% with a divided Congress, versus 12.0% for their Republican counterparts.” 2

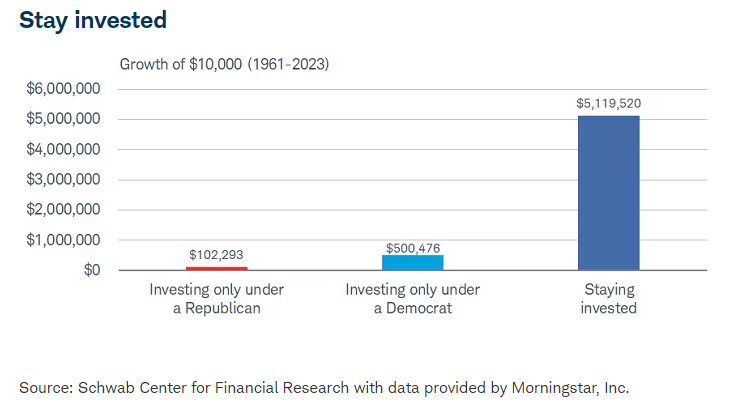

Another arguably counterintuitive lesson from history is that, when you remove the congressional make-up from the picture, the equity markets have surprisingly performed notably better under Democratic presidencies than Republican ones.

According to data from Morningstar, $10,000 invested in the Ibbotson U.S. Large Stock Index from January 2nd of 1961 through the end of 2023, but only invested during Republican presidencies would have grown to $102,293, while the same sum invested only during Democratic presidencies would have grown to over four times that amount or $500,476.

However, as is pointed out in that same report, to draw the conclusion that one should overweight stocks during Democratic administrations and underweight stocks during Republican administrations would miss the point entirely, as the $10,000 would have grown to a stunning $5,119,520, if it had remained fully invested through both Republican and Democratic administrations.

The lesson from history is that investors should largely ignore the political environment and stay invested (or at least not modify a portfolio allocation for purely political reasons).

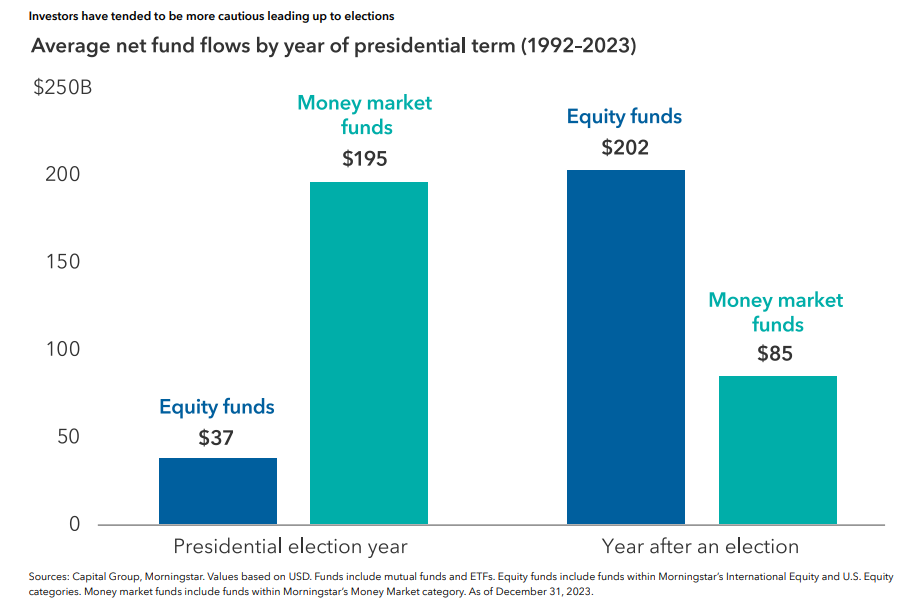

That is not to suggest that there are no idiosyncratic relationships between the political cycle and markets. For example, we previously noted that investors tend to hate uncertainty, and there is little doubt that election years introduce a whole new level of uncertainty into the investing environment, which helps to explain why investors have historically poured money into the safety of money market funds during election years, while greatly reducing new investment into the equity markets.

However, once election-year uncertainty is replaced by post-election clarity, investors have historically reversed course and shifted their investment flows from the safety of money market funds to the greater upside potential of stocks.

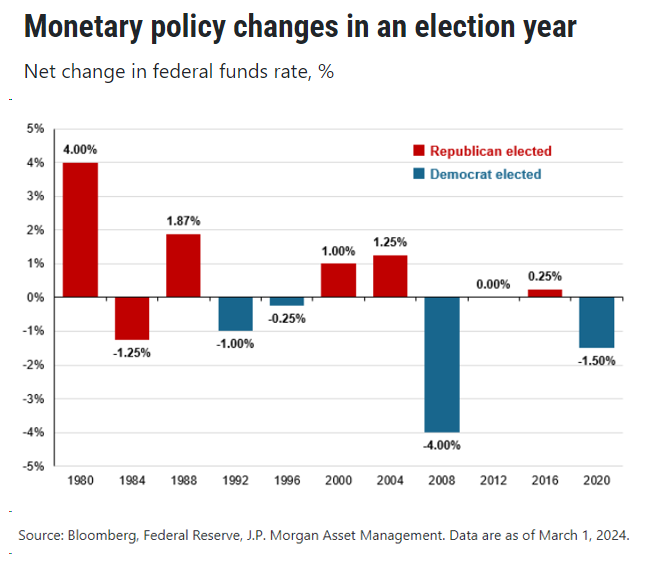

There is also a prevalent fallacy about the Federal Reserve during election years that we would like to address, as it could be of great importance this election year, when the Federal Reserve has made very clear their expectations that they will start lowering rates sometime in 2024.

The Federal Reserve operates as an independent agency of the Federal Government, and this independence is broadly accepted as being requisite for them to be able to effectively do their job.

This independence is granted to them by Congress. As such, the Fed has a long history of going to great lengths to avoid even the slightest suggestion of partisanship, which has led to a broadly held perception that the Federal Reserve will avoid making changes to monetary policy as we approach the elections, so to avoid any perception that they are trying to influence the outcome.

While this perception certainly makes sense, it is not borne out by history. As is shown in the above chart of monetary policy changes during election years, the Fed has sometimes been very active during election years, including two years (1980 and 2008) when they changed rates almost 80% as much as they did during the 2022-2023 period, which was the most aggressive rate hiking cycle in 40 years. The point being that Fed policy is likely to be driven by inflation, unemployment and economic growth rates, and not by the election calendar.

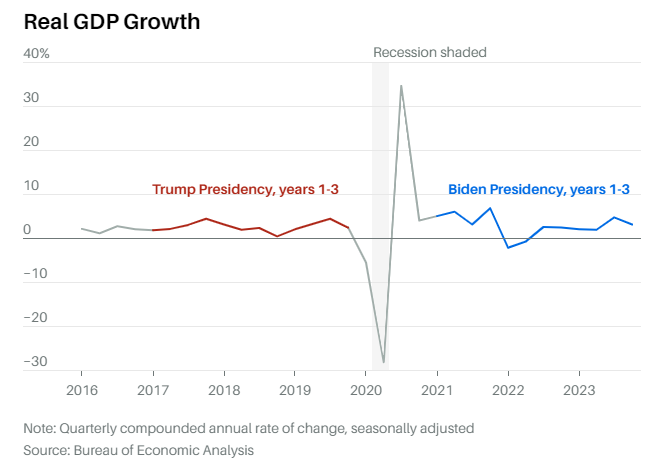

Having two former presidents running against each other is novel, to say the least, and it does provide a unique opportunity to compare the economy and markets during their respective terms. In this instance, this comparison is greatly complicated by the COVID pandemic, which caused a forced shut-down of the economy and massive fiscal and monetary policy stimulus that was far more impactful than any other policies coming out of either White House.

Nonetheless, Barron’s Magazine made an interesting attempt at lessening the influence of the pandemic by removing the February 2020 through December 2020 period from their calculations.

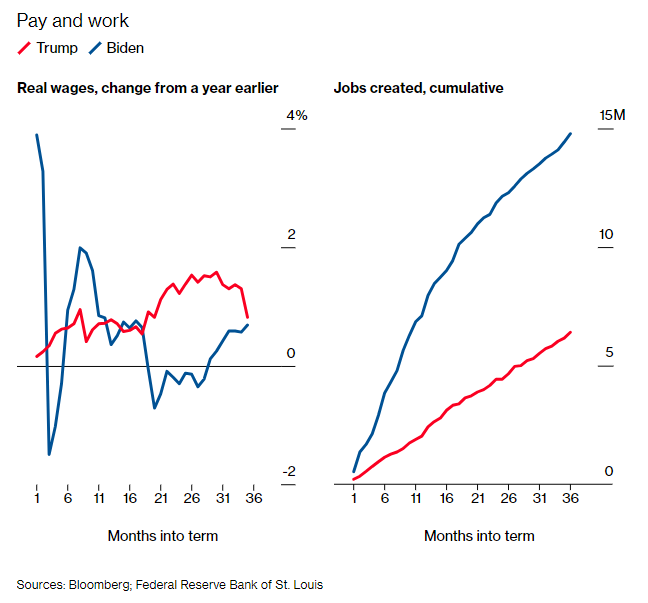

Doing so revealed that “real GDP, adjusted for inflation, averaged 2.6% during Trump’s first three years in office”. In contrast, “from Biden’s inauguration in January 2021 through the end of last year, real GDP grew by an average of about 3.4% a year.” Job creation was also much stronger under Biden. 3

That said, equity market returns were much stronger under Trump. According to that same Barron’s article, “from Trump’s inauguration in January 2017 through the end of 2019, the S&P 500 rose by 42.2%…[while]… Biden oversaw a jump of 23.8% in the S&P 500 from his inauguration through the end of 2023.”

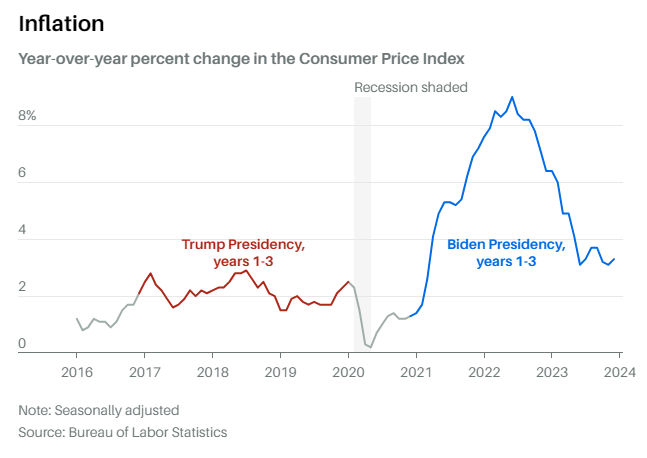

Inflation was much higher during the Biden presidency, but that was due primarily to the pandemic, the war in Ukraine, and the Fed being slow in its response to the surge in prices. Even so, it has had an indelible impact on the perception of Biden’s presidency and may be what ultimately cost him reelection.

In regard to the national debt, while both administrations were prolific spenders, Trump was by far the biggest offender. According to Barron’s, “Biden added $3.8 trillion to the national bill [while] Trump added $8.4 trillion to the debt… [Further, Trump’s] 2017 tax cuts are expected to add [an additional] $2.2 trillion in debt over a 10-year period.” 4

Importantly, this is an election that could push the bounds of historic precedent as, until fairly recently, Democrats were generally just left of center and most Republicans were just right of center. However, a combination of redistricting, gerrymandering, and the remarkable power of social media to add credibility to falsehoods and half truths has changed that dynamic in its entirety and, as a result, the more extreme elements of both parties are progressively driving their respective party agendas further and further away from the generally more centrist preferences and beliefs of the average American.

Similarly, the two presidential candidates have geometrically opposed platforms that are at least partially designed to appeal to these more extreme elements. As this presidential contest is anything but a choice between left-of-center and right-of-center, historic precedent could be less relevant than usual, and the outcome and consequences of this presidential cycle may be anything but normal or predictable.

President Biden’s proposed $7.3 trillion 2025 budget is full of new services and tax breaks for households earning less than $400,000, all paid for by new taxes on corporations and the wealthy. It includes a minimum tax on billionaires, that features a very problematic 25% tax on unrealized capital gains. For those making more than $1 million, all capital gains would be taxed at the much higher income tax rates (39.6% versus 20%) and wealthy taxpayers would also pay higher social security taxes.

The top corporate tax rate would jump from 21% to 28%, companies valued at $1 billion or more would pay a minimum tax rate of 21% and the tax that companies pay to do stock buybacks would quadruple. 5 Biden’s budget also calls for increasing the taxes that U.S. companies owe on foreign earnings to 21%, doubling the 10.5% rate in Trump’s tax law. 6

It would also eliminate the stepped-up cost basis on asset values when someone dies and would eliminate the 1031 exchange provision that allows for tax-free, like-kind exchanges between real estate properties. Biden’s proposal provides monthly tax credits to offset high mortgage rates and additional subsidies for childcare, while using the government’s negotiating power to lower the cost of prescription drugs.

Of course, as is the case with recent Republican proposals, just because the above changes are being proposed does not necessarily mean that they would pass through Congress.

A Biden reelection would also likely signal the expiration (sunsetting) of many of the provisions of Trump’s Tax Cuts and Jobs Act (TCJA) of 2017, which “lowered individual tax rates by restructuring the tax brackets, almost doubled the standard deduction from $13,000 to $24,000, decoupled the income threshold for capital gains taxes from ordinary income tax brackets to benefit higher-income taxpayers and effectively doubled the lifetime gift and estate tax exemption (from $5.6 million to $11.2 million)”. 7

In sharp contrast, former President Trump has promised the “biggest tax cuts” ever 8 and the proposed Republican budget makes the provisions of the 2017 Tax Cuts and Jobs Act permanent, while indexing capital gains, and repealing the estate tax outright. 9 While great for wealthy taxpayers, such a lack of fiscal discipline would likely further exacerbate the deficit at a time when Fed Chairman Powell has already proclaimed that “the U.S. is on an unsustainable fiscal path”. 10

In addition, Trump has already stated that he would be replacing Fed Chairman Powell at the end of Powell’s term, and all indications are that Trump would sacrifice the Fed’s independence by replacing him with someone who would take directions from the White House.

When you throw in Trump’s promise to impose “a baseline 10% tariff on all U.S. imports and a levy of 60% or higher on imported Chinese products”, 11 it introduces a new risk that the resulting surge in inflation could reverse much of the Fed’s recent progress, and even force them into making additional rate increases.

As was just noted by research firm Capital Economics, “his tariff proposals would probably trigger a rebound in inflation which could persuade the FOMC [i.e., the Fed’s Federal Open Market Committee] to raise interest rates. So, while the source of the inflation impulse would be different (tariffs rather than concerns over expansionary fiscal policy), we think that a win for Trump would once again push up Treasury yields…Such an increase in ‘risk-free’ discount rates would weigh on equity valuations, all else equal. What’s more, we think the proposed tariffs could subtract up to 1.5% from US GDP, weighing on corporate earnings expectations.” 12

J.P. Morgan chief market strategist Marko Kolanovic recently offered a similarly cautious view of the upcoming elections: “Our view is that there is likely no market upside related to November’s election; the outcome is either status quo (incumbent party stays in power), or increased uncertainty related to global trade and geopolitical or domestic tensions.” 13

While neither of the presumed candidates for president is particularly compelling when viewed purely from the perspective of an investor, we take some comfort from our overall premise that the political environment, at least from a historical perspective, has been much less impactful on the performance of the capital markets than many other factors.

In addition, we think that the odds are high that the election will once again produce an outcome of divided government, a president with low approval ratings, and that political dysfunction is likely a foregone conclusion. In the current environment of resilient economic growth, generally declining inflation, and improving corporate profits, political inefficacy might be all that stocks need to sustain the current uptrend into the new year. In general, we think that portfolio values should continue their post-COVID recovery for as long as political dysfunction persists and keeps whoever we elect in November from working together and potentially “making things worse”.

Disclosures

Advisory services offered through Per Stirling Capital Management, LLC. Securities offered through B. B. Graham & Co., Inc., member FINRA/SIPC. Per Stirling Capital Management, LLC, DBA Per Stirling Private Wealth and B. B. Graham & Co., Inc., are separate and otherwise unrelated companies.

This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation or advice of any kind. The information contained herein may contain information that is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor.

This document may contain forward-looking statements based on Per Stirling Capital Management, LLC’s (hereafter PSCM) expectations and projections about the methods by which it expects to invest. Those statements are sometimes indicated by words such as “expects,” “believes,” “will” and similar expressions. In addition, any statements that refer to expectations, projections or characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Such statements are not guarantying future performance and are subject to certain risks, uncertainties and assumptions that are difficult to predict. Therefore, actual returns could differ materially and adversely from those expressed or implied in any forward-looking statements as a result of various factors. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the views of PSCM’s Investment Advisor Representatives.

Neither asset allocation nor diversification guarantee a profit or protect against a loss in a declining market. They are methods that can be used to help manage investment risk.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted.

Definitions

The Standard & Poor’s 500 (S&P 500) is a market-capitalization-weighted index of the 500 largest publicly-traded companies in the U.S with each stock’s weight in the index proportionate to its market. It is not an exact list of the top 500 U.S. companies by market capitalization because there are other criteria to be included in the index.

Real gross domestic product (GDP) is a comprehensive measure of U.S. economic activity. GDP measures the value of the final goods and services produced in the United States (without double counting the intermediate goods and services used up to produce them). Changes in GDP are the most popular indicator of the nation’s overall economic health.

The Consumer Price Index (CPI), which is produced by the Bureau of Labor Statistics, is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Indexes are available for the U.S. and various geographic areas. Average price data for select utility, automotive fuel, and food items are also available.

Citations

-

“The Interplay: Presidential Approval Ratings and Market Performance”, Advisorpedia, Posted 3/8/2024, https://www.advisorpedia.com/chart-center/the-interplay-presidential-approval-ratings-and-market-performance/

-

“A Trump win: A ticking time bomb for the bond market”, Nuria Salobral, As of 2/26/2024, https://www.msn.com/en-ie/money/markets/a-trump-win-a-ticking-time-bomb-for-the-bond-market/ar-BB1iUalF

-

“The Trump vs. Biden Economy: A Comparison in 10 Charts”, Megan Leonhardt, Posted 2/25/2024, https://www.barrons.com/articles/trump-biden-economy-inflation-presidential-race-f8c52941

-

“The Trump vs. Biden Economy: A Comparison in 10 Charts”, Megan Leonhardt, Posted 2/25/2024, https://www.barrons.com/articles/trump-biden-economy-inflation-presidential-race-f8c52941

-

“Capital Gains Hikes at Center of Biden’s Second-Term Tax Agenda”, Laura Davison, Lauren Vella, and Erin Schilling, Posted 3/11/2024, https://www.msn.com/en-us/money/other/capital-gains-hikes-at-center-of-biden-s-second-term-tax-agenda/ar-BB1jHZ6Q?ocid=hpmsn&pc=AV01&cvid=5581d958349e4cef98ab4588f58c7cf9&ei=13

-

“10 Big Tax Fights Lurking in Biden-GOP Budget Faceoff”, John Manganaro, Posted 3/21/2024, https://www.thinkadvisor.com/2024/03/21/10-big-tax-disagreements-in-biden-gop-budget-plans/?kw=10%20Big%20Tax%20Fights%20Lurking%20in%20Biden-GOP%20Budget%20Faceoff&utm_position=1&utm_source=email&utm_medium=enl&utm_campaign=weekendreview&utm_content=20240323&utm_term=tadv&oly_enc_id=2348C2818612H6W&user_id=0ac6a7c7db477217b2e779ee530cfffaa8e8e51c7cb35a55a83df6b664ccdc43

-

“What to Do Before the Tax Cuts and Jobs Act Provisions Sunset”, Martin Schamis, Posted 6/13/2023, https://www.kiplinger.com/taxes/what-to-do-before-tax-cuts-and-jobs-act-tcja-provisions-sunset

-

“Capital Gains Hikes at Center of Biden’s Second-Term Tax Agenda”, Laura Davison, Lauren Vella, and Erin Schilling, Posted 3/11/2024, https://www.msn.com/en-us/money/other/capital-gains-hikes-at-center-of-biden-s-second-term-tax-agenda/ar-BB1jHZ6Q?ocid=hpmsn&pc=AV01&cvid=5581d958349e4cef98ab4588f58c7cf9&ei=13

-

“10 Big Tax Fights Lurking in Biden-GOP Budget Faceoff”, John Manganaro, Posted 3/21/2024, https://www.thinkadvisor.com/2024/03/21/10-big-tax-disagreements-in-biden-gop-budget-plans/?kw=10%20Big%20Tax%20Fights%20Lurking%20in%20Biden-GOP%20Budget%20Faceoff&utm_position=1&utm_source=email&utm_medium=enl&utm_campaign=weekendreview&utm_content=20240323&utm_term=tadv&oly_enc_id=2348C2818612H6W&user_id=0ac6a7c7db477217b2e779ee530cfffaa8e8e51c7cb35a55a83df6b664ccdc43

-

“Powell Warns of ‘Unsustainable’ Fiscal Path, Talks Rate Cuts”, Joshua Roberts, Posted 2/5/2024, https://finance.yahoo.com/news/powell-warns-unsustainable-fiscal-path-234745282.html

-

“Here’s what Trump’s proposed tariffs could mean for your wallet”, Kate Dore, Posted 3/13/2024, https://www.cnbc.com/2024/03/13/heres-what-trumps-proposed-tariffs-could-mean-for-your-wallet-.html

-

“Market implications of Trump 2.0”, Capital Economics, Posted 2/22/2024, https://www.capitaleconomics.com/publications/global-markets-focus/market-implications-trump-20

-

“The Election Is Coming. These Stock Sectors Tend to Perform Best.”, Joe Light, 2/26/2024, https://www.barrons.com/articles/trump-biden-election-stock-sectors-c1e66112